Anti-Subsidies Duties on Chinese EVs: Who Bears the Cost?

On 20th January 2025, Donald Trump will become the American President for the second time, and it is expected that a new trade war involving all Chinese goods will start soon. Although this protectionist movement was initiated in the first Trump period, the Biden Administration also inflicted a blow against Chinese manufacturers of semiconductors, solar cells, electric vehicles (EVs), lithium-ion EV batteries, steel, and aluminium this year. This episode serves as an instructive case study of the adverse impacts of industry protection, which, in this case, involves imposing costs on consumers and slowing the takeup rate of EVs in the US.

China has recently become the ‘leading’ exporter and top world manufacturer of EV passenger vehicles. This year, Chinese producers of EVs were affected by two unilateral trade measures imposed by the United States (US) in May and the European Union (EU) in July (a definitive tariff for five years was imposed later in October). Both ‘countervailing duties’ (also known as ‘anti-subsidies duties’)1 increased import tariffs on EVs (the US quadrupled its tariffs from 25% to 100%, while the EU raised tariffs from 10% to 35.3%). The US and the EU believe that the Chinese government is granting subsidies to its EV industry, creating an unfair competitive advantage to the detriment of American and European car manufacturers2. This article analyses how both measures affect major economic players using some elements of international trade theory.

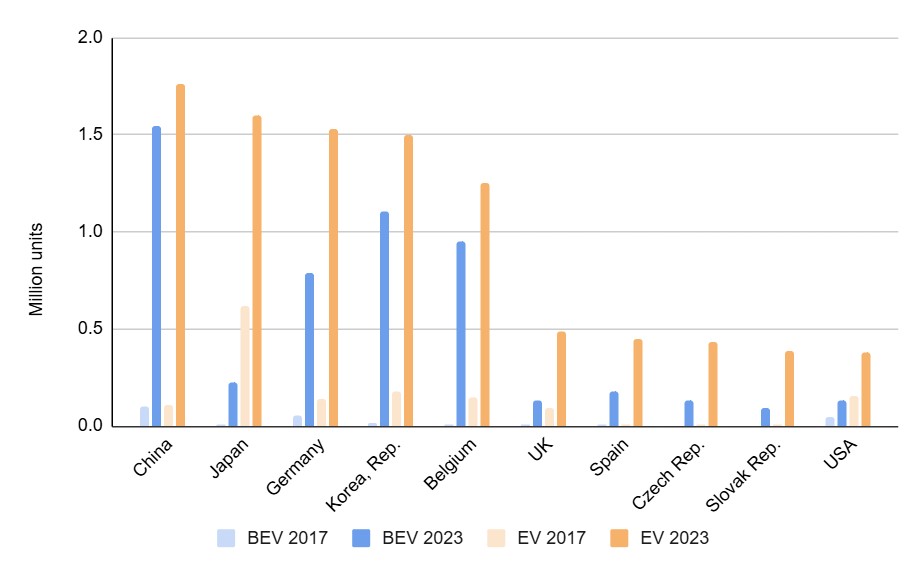

The Chinese EV industry is leading the global market in EV sales due to the major production of Battery Electric Vehicles (BEV). Figure 1 shows that China exported more EV units than other car manufacturing countries in 2023, registering 1.76 million units shipped to the rest of the world, followed by Japan with 1.59 million units and Germany with 1.53 million units. Six years ago, China was behind Japan, South Korea, the US, Belgium, and Germany, among other countries. Regarding BEV, China has kept its supremacy as the major BEV exporter since 2017, which could be associated with Chinese technological innovations in lithium batteries, the most costly input for fully electric vehicles3.

Figure 1. Top ten exporters of EVs by million units

Source: World Trade Organisation (WTO) Secretariat (2024)

On the import side, Figure 2 shows that the United States was the largest individual destination market for EVs, representing 14.3% of global EV imports (USD 305.6 billion) in 2023, followed by Germany (9.2%), the UK (8.6%), Belgium (8.0%), and France (6.1%), among others. Regarding BEVs, the US is the leading buyer, with 12.9% of global BEV imports (USD 147.6 billion) in 2023, followed by Germany (10%), the UK (10%), Belgium (8.7%), and France (6.4%), among others.

Figure 2. Top ten importers of EVs by USD billion

Source: WTO Secretariat (2024)

Regarding import tariffs on EVs, the World Trade Organisation (WTO) Secretariat (2024) indicated that most WTO members (around 55 countries) apply Most Favoured Nation (MFN) tariffs4 on BEVs lower than 15%, while 36 WTO members applied import duties greater than 15% on BEVs (see Table 1). In Australia, imported electric vehicles, plug-in hybrid vehicles and hydrogen fuel-cell vehicles with a customs value less than the fuel-efficient luxury car threshold ($91,387 for 2024-25) are duty-free. The WTO secretariat (2024) pointed out that “this tariff structure suggests that some WTO members are orienting policies to promote the adoption of battery and hybrid EVs in preference to internal combustion engine cars, while other members do not differentiate their tariff treatment and may instead using other types of policies, such as subsidies or technical regulations to promote such adoption”.

Table 1. Number of WTO members by Most Favoured Nation (MFN) applied tariff range and type of electric engine

Source: WTO Secretariat (2024)

However, the US and the EU have imposed anti-subsidies duties on Chinese EVs to protect their domestic industry against what are considered unfair Chinese subsidies5. Scott Kennedy, Senior Adviser and Trustee Chair in Chinese Businesses and Economics of The Center for Strategic and International Studies, pointed out that “China’s trading partners argue that these tensions are the result of Chinese industrial policy and unfair trade practices. China argues that its growing exports reflect the country’s natural advantage and the high quality of its companies’ products. The reality – and what makes this a difficult challenge – is that there is some truth in both perspectives”.

China is not the only country that has been subsidising its EV industry. Indeed, the US Department of Energy has provided grants to support EV manufacturing and its supply chain. Also, Japan is addressing the dominance of Chinese EVs by investing heavily in solid-state battery technology, aiming to bypass China’s control over lithium-ion battery supply chains. Through government funding (i.e. subsidies for R&D initiatives), cutting-edge research, and global partnerships, Japanese manufacturers are working to secure a competitive edge in the EV market.

According to Stephen Ezell, the Vice President of Global Innovation Policy at the Information, Technology and Innovation Foundation (ITIF), China has a first-mover advantage due to its dominance in EV battery production, representing almost 40% of production EV’s value. This dominance was obtained by investing early in battery technology research, upstream mineral mining and refining, and other EV technological capabilities. Moreover, Shiv Shivaraman, Partner and Managing Director, Co-Leader Asia of AlixPartners, indicated that “…EVs sell in China for the equivalent of $34,400, considerably lower than the $55,542 average selling price in the US. Many factors drive this disparity. Chinese automakers have a notable cost advantage due to lower labour rates, increased scale, healthy government subsidies, and more favourable battery costs (many of the world’s EV batteries or components are sourced from China).”

The 2008 Nobel Prize winner, Paul Krugman, developed the New Trade Theory (NTT) in the late 1970s and early 1980s, explaining how economies of scale and network effects play a significant role in international trade. Unlike traditional trade theories, which focus on comparative advantage, NTT suggests that countries can gain an advantage by specialising in producing certain goods, even without clear cost advantages, because large-scale production reduces costs. This allows firms in countries with similar factor endowments to trade with each other, benefiting from an increased variety of products and lower prices for consumers. The theory also explains how early entry into industries can give firms a competitive edge, creating “first-mover advantages”.

These first-mover and cost advantages make early EV manufacturers highly competitive, allowing them to gain market share in other countries quickly. Economically powerful and well-organised industrial groups could pressure governments to implement trade measures (e.g. additional anti-subsidies tariffs) to protect their stakes. On the other hand, consumers, especially those with low incomes, will be the most negatively affected by those additional tariffs because they will need to pay more for cheaper EVs and have fewer varieties of cars to choose from because the EV importers will need to charge higher prices, incorporating partially or wholly additional costs of the anti-subsidies tariffs.

In environmental terms, these trade measures may inadvertently hinder green initiatives by limiting access to affordable EVs, which are crucial for reducing carbon emissions. For example, Chinese BEV manufacturers, such as BYD, offer models like the Seagull at approximately US$11,500, featuring a 250-mile (402.3 km) range. In contrast, the US market’s most affordable EV, the Nissan Leaf, starts at around US$29,000 with a 149-mile (239.8 km) range. Henry Lee, the Jassim M. Jaidah Family Director of Harvard School’s Environmental and Natural Resources Program, noted that by restricting these Chinese clean energy alternatives, the tariffs could slow the adoption of EVs among American consumers, thereby impeding efforts to decarbonise the transportation sector.

The challenges posed by the new anti-subsidy tariffs underscore the complexity of integrating trade policy with environmental imperatives. Policymakers must strike a balance that fosters innovation, protects domestic industries, accelerates the global shift toward sustainable transportation solutions, and provides a greater variety of goods to consumers. As Japan’s investment in cutting-edge battery technology demonstrates, strategic responses to market dominance can foster competition without the adverse effects of trade restrictions. This is important because consumers in Japan will not be affected by protectionist measures, which can do more harm than good.