Coffee’s economic contribution in Australia

Over 27-30 September 2022, Melbourne will host the World Coffee Championships, attracting the attention of coffee connoisseurs around the world. Australia is well known for its coffee culture and the skill of our baristas. With the World Coffee Championships this week, we thought it would be useful to survey the coffee market in Australia and the economic and employment opportunities it provides. Certainly, those opportunities are substantial. For instance, in 2021-22, cafes and coffee shops employed over 142,100 people, 0.3% higher than the previous financial year, and paid $2.75 billion in wages and salaries.

Australian coffee consumption

Australians consumed approximately 2.1 kg of coffee per capita in 2021 (1). Two-thirds were consumed as instant coffee, and one-third as roasted coffee (e.g. percolator, plunger, or espresso machine). Australia’s coffee consumption is not particularly high, compared with over 10kg per capita in Sweden and Finland (see this BBC News report).

A survey conducted by McCrindle showed that three out of four Australians drink at least one cup of coffee, and 28% of those coffee drinkers consumed three or more cups per day in 2017. Australian coffee consumers can be largely divided into those who prefer drinking instant coffee (39%) and those who prefer drinking espresso (39%). The rest prefer other types of coffee drinks.

The global coffee market

Coffee is traded in a large global market. The global price for coffee beans reached US 255.43 cents/lbs on 09 February 2022. After that peak, prices declined to about US 220.4 cents/lbs on 23 September 2022, which is still substantially higher than the US 100-150 cents/lbs range coffee was usually trading in during the second half of the last decade. This is one of the reasons, along with other inflationary pressures, why the price of a cup of coffee has increased significantly in Australia in 2021-22. On 1 August 2022, ABC News reported a Queensland coffee industry player saying that “A coffee that used to cost $5 is now probably $6.”

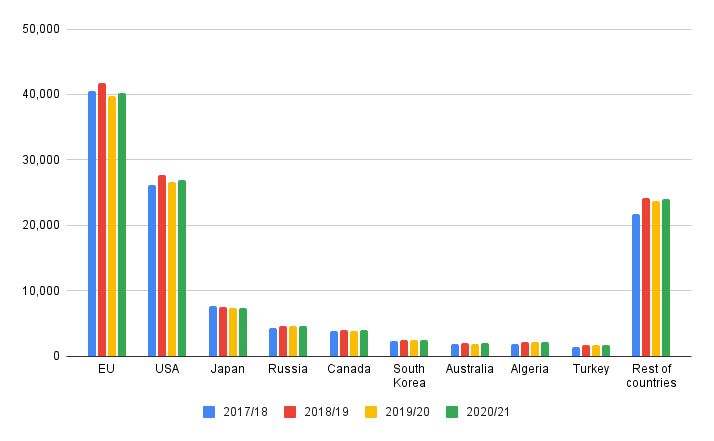

Figure 1 shows that the major coffee importers were the European Union with 35% of total imports worldwide in the 2020-21 coffee year (October to September), the United States with 23%, and Japan with 6%. Australia ranked in the sixth position with almost 2% of total imports and with an average annual growth rate of 1.9% since 2018-19.

Figure 1. World’s major coffee importers (in thousand 60kg bags)

Source: International Coffee Organisation. Prepared by Adept Economics.

Australian coffee products: What are their sources?

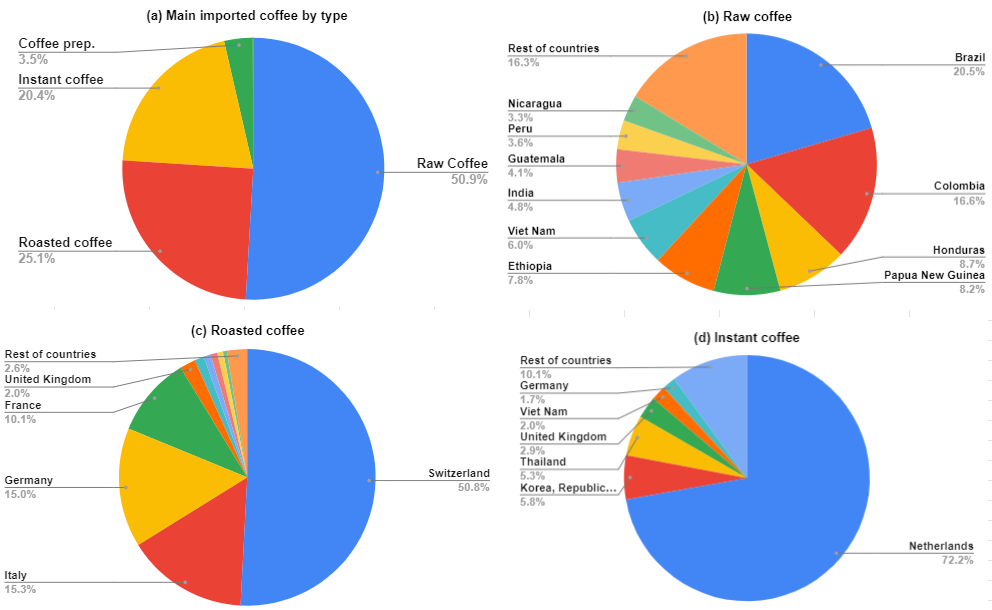

The vast bulk of the coffee beans that Australians ultimately consume are imported. Local-grown coffee contributes only around 1% to coffee consumption in Australia. Australian imports of coffee include both inputs for processing (e.g. roasting) and final products to be sold in retail stores. Coffee imports include raw coffee beans, roasted coffee beans, instant coffee, and other preparations containing coffee. Imports of coffee into Australia amounted to 669 million USD (i.e. approximately $900 million) in 2021. The most relevant imported product was raw or green coffee beans at 50.9% of Australian total coffee imports in 2021, followed by roasted coffee beans at 25.1%, and instant coffee at 20.4% (see Figure 2.a).

The main countries that were sources of raw coffee for Australia were Brazil (20.5%) and Colombia (16.6%), which together represented over one third of total raw coffee imports in 2021 (see Figure 2.b, 2c and 2.d). Overall, Australian producers (roasters and instant coffee makers) bought raw coffee from suppliers from 52 different countries in 2021. With respect to roasted coffee, Switzerland (51%), Italy (15%), Germany (15%) and France (10%) were the main competitors for Australian roasters (e.g. Merlo and Campos). In the case of instant coffee, the Netherlands (72%) was the major country from which imports were sourced. The Netherlands is the production centre of Moccona-producer Douwe-Egberts.

Figure 2. Australian imports by type of coffee and its main sources in 2021 (USD)

Source: Trade Map. Prepared by Adept Economics. Note: These categories include corresponding decaffeinated products. Moreover, “prep.” denotes preparations.

Australian coffee industry

A substantial amount of coffee consumed in Australia is roasted in Australia and some of it is manufactured as instant coffee here in Australia. The Tea and Coffee Manufacturing industry in Australia had revenue of $1.66 billion in 2021-22 according to IBISWorld. Unfortunately, a split of the revenue estimate between tea and coffee manufacturing is unavailable.

The Australian coffee manufacturing industry is highly competitive in price, quality, and range. According to IBISWorld, the main activities in the coffee manufacturing industry are coffee processing for instant coffee (52% of total revenue), coffee beans and grounds (34% of total revenue), and coffee capsules (14% of total revenue). Most roasters and processors primarily use imported raw coffee beans and instant coffee to make roasted coffee and instant coffee blends. For example, Nescafe Blend 43 is roasted and blended in Gympie, Queensland, using imported raw ingredients.

IBISWorld points out that the major players in processing coffee in the last five years in Australia were Jacobs Douwe Egberts (20% of total coffee and tea manufacturing revenue), Nestle (12%), Vittoria Food and Beverage (12%), and Unilever Australia (7%), with an assortment of other companies making up the bottom half of the market.

Encouragingly, the number of micro-roasting companies has soared in major Australian cities. Examples of micro-roasting companies include Elixir at Stafford, Brisbane, Black Market Roaster at Marrickville, Sydney, and Rumble Coffee at Kensington, Melbourne. Additionally, there are roasters who will roast for independent coffee companies which do not own their own roasters. For example, the Coffee Commune in Brisbane has a bean roasting service for coffee businesses and cafes so they can market their own blends, and it offers further support to those businesses to help them become more efficient and sustainable.

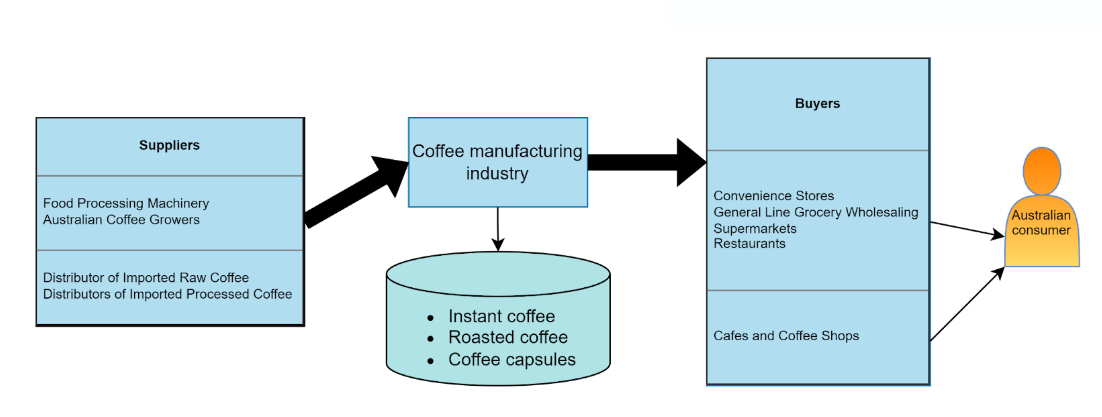

Grocery stores, restaurants, cafes and coffee shops, and supermarkets are the intermediaries between coffee manufacturers and final consumers in the Australian domestic market (see Figure 3). The pattern of coffee consumption is shifting towards specialties such as roasted premium and blended coffee beans. Broadly speaking, younger Australians prefer to consume more sophisticated coffee products than older Australians. Additionally, more households are consuming coffee capsules, such as Nespresso pods, due to a greater variety of coffees and the proliferation of cheaper capsule machines.

Figure 3. Simplified coffee supply chain

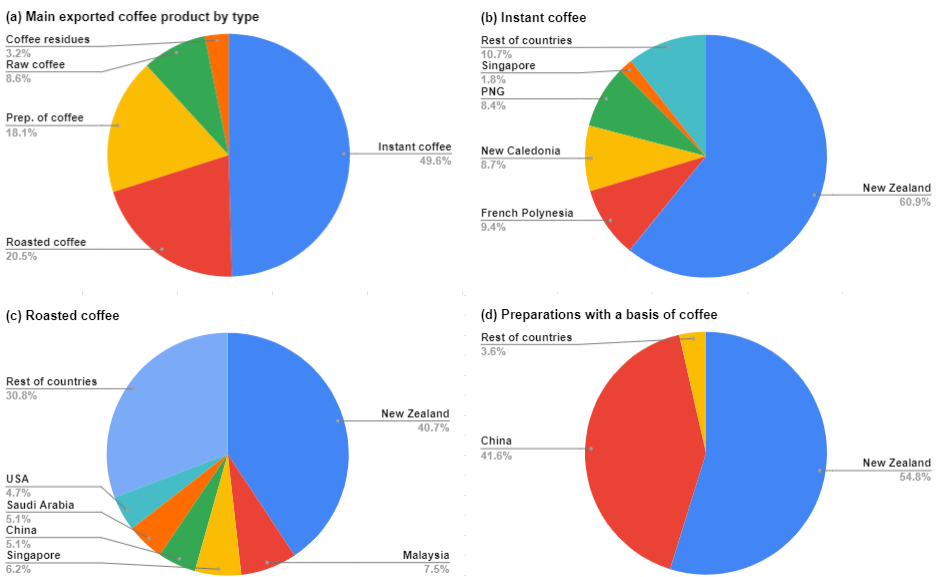

The Australian coffee industry also exports part of its production to overseas markets. Australian coffee exports reached 64.4 million USD, an amount equivalent to only 10% of Australia’s total coffee imports, in 2021. The main types of exported coffee products are instant coffee (including decaf) with 50% of the total, roasted coffee with 20%, and preparations containing coffee with 18% (see Figure 4.a). The major destination market for Australian coffee across all categories is New Zealand: 61% of instant coffee, 40.7% of roasted coffee, and 54.8% of preparations containing coffee.

Figure 4. Australian exports by type of coffee and its destinations markets in 2021 (USD)

Source: Trade Map. Prepared by Adept Economics.

According to IBISWorld, the Australian coffee (and tea) manufacturing industry is expected to keep growing at around 0.5% in revenue terms annually over the next five years. This is mainly underpinned by the rising demand for coffee products such as premium coffee and coffee capsules. With respect to employment, Australia’s coffee (and tea) manufacturing industry employed approximately 4,900 workers in 2021-22, 4.5% higher than the previous financial year.

Growth of cafes and coffee shops

An important factor that underpinned the growing trend toward coffee specialties is the strong coffee culture in Australia, supporting the proliferation of cafes and coffee shops across the country. In 2021-22, Australia had around 28,700 cafes and coffee shops. While some cafes closed down during COVID-19, particularly in CBDs, in many cases new ones have opened up in the same locations or in the suburbs.

The market structure for cafes and coffee shops in Australia can be described as close to perfect competition, given the presence of small and individual businesses and low barriers to entry. There is a large number of well-informed consumers, prompting cafes and coffee shops to set highly competitive prices.

That said, some cafes can develop a reputation for producing superior flat whites or lattes and charge premium prices. Also, some cafes, such as those in airports, benefit from location monopolies which allow them to charge above market prices.

On the consumer side, as noted above, many Australians are seeking out premium coffees, including fair trade and organic varieties. Australians continue to love drinking coffee and, with a growing population, the market is expected to keep growing. That said, in the short-term, there is a potential threat from currently high traded coffee prices and other inflationary pressures that are affecting profits margins in smaller cafes and coffee shops.

What about the future?

This year the industry has been adversely affected by a worldwide shortage of coffee beans and hence rising coffee bean prices, at the same time as fuel prices have surged. Despite the short-term disruption, the long-term outlook is positive. Australian coffee production will keep increasing due to the solid demand for coffee products boosted by the many factors discussed in this article. It seems that the pattern of consumption will keep shifting towards coffee specialties (e.g. espresso, coffee capsules, and ground coffee and beans), further decreasing the market share of instant coffee. In addition to that, overseas demand for Australian processed coffee will likely rise steadily, specifically in Asia.

Australia’s vibrant coffee culture will continue to play a role in fostering overseas demand for Australian coffee products. Indeed, Australia is exporting our cafe culture around the world. Bluestone Lane, an Australian cafe and coffee shop brand, has more than seventeen stores dispersed across the United States, promoting the way that Australians enjoy a cup of coffee. The future looks bright for the Australian coffee industry.

Published 26 September 2022 and modified 24 December 2024. This article was prepared by Adept Economics Research Economist Arturo Espinoza and Director Gene Tunny. Please email us via contact@adepteconomics.com.au if you have any questions or comments. Alternatively, please call us on 1300 169 870.